![[Image by creator from ]](/media/images/patrick-lunsford.2e16d0ba.fill-500x500.jpg)

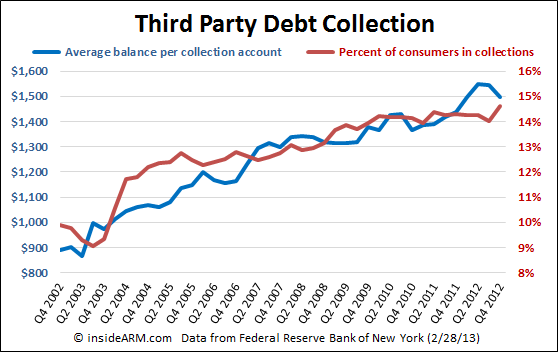

The percentage of Americans with at least one account in third party collections rose to an all-time high in the fourth quarter of 2012, according to the Federal Reserve Bank of New York. The average account balance of those in collection decreased.

In its Quarterly Report on Household Debt and Credit for the fourth quarter of 2012, the Federal Reserve Bank of New York (FRBNY) noted that 14.6 percent of American consumers had an account in the third party debt collection system, up from 14 percent in the third quarter. Since peaking at 14.38 percent in the second quarter of 2011, the percentage of consumers in collections had steadily fallen. But the spike in the number for the fourth quarter shattered the old record.

While more Americans find themselves with a third party debt collection account, the average balance on those accounts fell in the quarter. The FRBNY reported that the average balance per collection account fell to $1,499 in Q4 2012 from $1,546 in the previous quarter.

The Quarterly Report on Household Debt and Credit is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative random sample drawn from Equifax credit report data.

Total consumer indebtedness was $11.34 trillion, 0.3 percent higher than the previous quarter but considerably lower than its peak of $12.68 trillion in the third quarter of 2008. While outstanding mortgage debt remained roughly flat, originations of new mortgages rose to $553 billion, a fifth consecutive quarterly increase.

Non-housing debt balances increased for the third straight quarter and now stand at $2.75 trillion, up 1.3 percent in the fourth quarter. All non-housing components increased; auto loans up $15 billion, student loans up $10 billion and credit cards up $5 billion.

“The data provides early evidence that consumers may be reaching the end of the four year deleveraging cycle, though we’ll need to see if this is sustained in upcoming quarters,” said Andrew Haughwout, vice president and economist at the New York Fed. “At the same time, we observed mixed developments, mortgage originations increased and fewer accounts entered the foreclosure pipeline but delinquency rates remain considerably higher than pre-crisis levels.”

Outstanding student loan debt now stands at $966 billion, an increase of $10 billion from last quarter. The percent of student loan balances 90+ days delinquent increased again and currently stands at 11.7 percent.

Other highlights from the report include:

- 8.6 percent of total debt was in some stage of delinquency compared with 8.9 percent the previous quarter.

- Outstanding auto loans ($783 billion) are the highest in nearly four years.

- Delinquency rates for mortgages improved to 5.6 percent from 5.9 percent the previous quarter.

- Delinquency rates for home equity lines of credit, which stood at 4.9% in the third quarter, dropped to 3.5 percent; a decline primarily reflecting higher charge-offs of delinquent HELOCs this quarter.

- About 210,000 individuals had a new foreclosure notation added to their credit report, a quarterly slowdown of 13.3 percent, continuing a downward trend.

![the word regulation in a stylized dictionary [Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.png)

![Cover image for New Agent Onboarding Manuals resource [Image by creator from insideARM]](/media/images/New_Agent_Onboarding_Manuals.max-80x80_3iYA1XV.png)

![[Image by creator from ]](/media/images/New_site_WPWebinar_covers_800_x_800_px.max-80x80.png)

![[Image by creator from ]](/media/images/Finvi_Tech_Trends_Whitepaper.max-80x80.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![Webinar graphic reads RA Compliance Corner - Managing the Mental Strain of Compliance 12-4-24 2pm ET [Image by creator from ]](/media/images/12.4.24_RA_Webinar_Landing_Page.max-80x80.png)